Non-Resident TDS Update from April 1, 2026: Complete Guide to New Rules, Rates & Compliance Under the Income Tax Act, 2025.

Comprehensive guide to new Non-Resident TDS rules effective April 1, 2026. Learn Section 393(2), updated rates, DTAA benefits, compliance requirements, and risk areas under the Income Tax Act, 2025.

Introduction: A Structural Shift in Non-Resident TDS Framework

India’s taxation landscape for cross-border transactions has undergone a notable transformation with the introduction of the Income Tax Act, 2025, replacing and modernizing legacy provisions of the earlier law. One of the most critical changes is the overhaul of Tax Deducted at Source (TDS) provisions applicable to non-residents, effective April 1, 2026.

The new framework aims to simplify compliance, align with global taxation standards, and enhance transparency while maintaining robust reporting and withholding mechanisms.

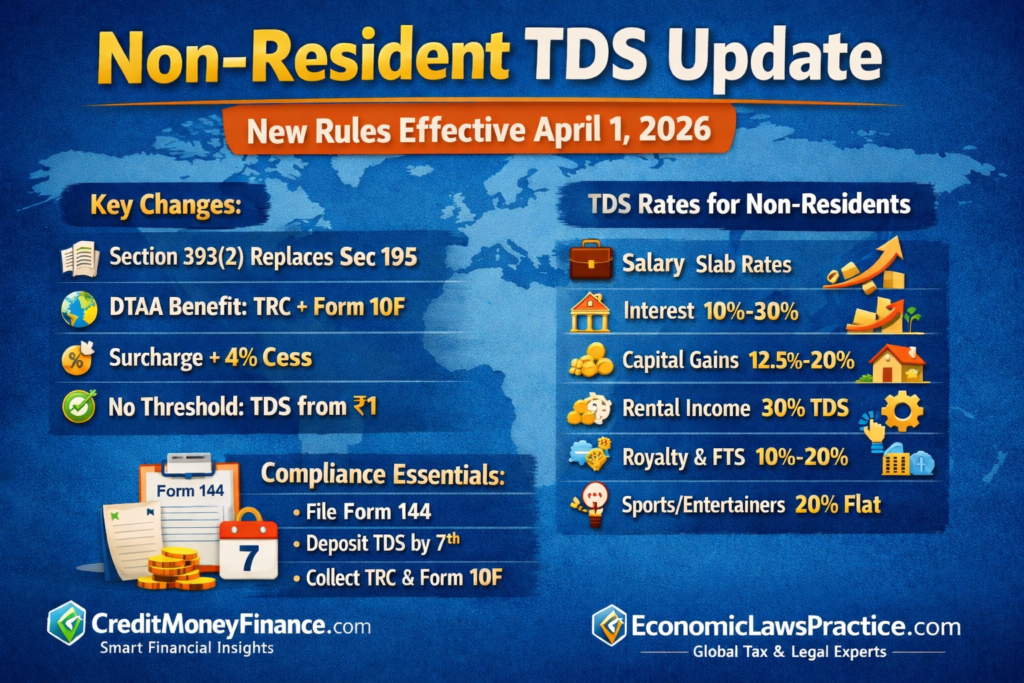

Section 393(2): The New Backbone of Non-Resident TDS

The most significant reform is the introduction of Section 393(2), which replaces the widely used Section 195 of the earlier Income Tax Act.

Under this provision:

- Any person responsible for making payment to a non-resident must deduct TDS

- Applies to any sum chargeable to tax in India

- Continues the principle of “withholding at source” but with updated compliance procedures

While the core concept remains unchanged, the structure, forms, and reporting mechanisms have been modernized for better efficiency and tracking.

TDS Rates for Non-Residents (FY 2026-27)

Although the compliance framework has evolved, TDS rates remain broadly consistent with previous provisions. However, applicability depends heavily on the nature of income and treaty benefits.

1. Salary Income (Section 392)

TDS is deducted as per applicable income tax slab rates. Employers must consider:

- Residential status

- Duration of stay

- Applicable deductions and exemptions

2. Interest Income

TDS ranges between 10% to 30%, depending on:

- Type of interest (e.g., NRO deposits, ECBs)

- Applicable surcharge and cess

- DTAA relief, if claimed

3. Capital Gains

- Short-term gains: Typically 15% to 20%

- Long-term gains: Around 12.5% (subject to conditions)

TDS must be deducted at the time of transfer, even if the actual gain is uncertain.

4. Rental Income

- Flat 30% TDS on gross rental income

- No deduction allowed for expenses at withholding stage

This often leads to higher TDS than actual tax liability, requiring refund claims.

5. Royalty & Fees for Technical Services (FTS)

- TDS rate: 10% to 20%

- Subject to DTAA provisions, which may reduce the rate

6. Income of Sportsmen & Entertainers

- Flat 20% TDS

- Applicable to income earned from performances, endorsements, or appearances in India

Surcharge and Health & Education Cess

- Applicable in addition to base TDS rates

- 4% Health & Education Cess applies in most cases

- Surcharge rates vary depending on income level

However, when DTAA benefits are applied, surcharge and cess may not be applicable, depending on treaty terms.

DTAA Benefits: Critical for Tax Optimization

India has Double Taxation Avoidance Agreements with multiple countries, allowing reduced TDS rates or exemptions.

To claim DTAA benefits, the following documents are mandatory:

- Tax Residency Certificate (TRC)

- Form 10F

- Declaration of Beneficial Ownership

Failure to provide these documents leads to higher domestic TDS rates, increasing cash flow burden.

No Threshold Limit: TDS from ₹1

A key compliance shift is the absence of any minimum threshold limit.

- TDS is applicable from the first rupee

- Even small payments to non-residents require withholding

This significantly increases compliance responsibility for businesses making cross-border payments.

New Compliance Framework Under the 2025 Act

1. Introduction of Form 144

- Replaces Form 27Q

- Used for reporting TDS on payments to non-residents

2. TDS Certificate Requirements

- Must reflect new section codes (393(2))

- Timely issuance is mandatory

3. TDS Payment Timeline

- Deposit TDS by 7th of the following month

- For March transactions: Deadline is April 30

4. Lower or Nil TDS – Form 13

Taxpayers can apply for reduced TDS deduction using Form 13, especially in cases where:

- Actual tax liability is lower

- Losses or exemptions are available

5. Documentation Before Remittance

Before making payment to non-residents, ensure collection of:

- TRC

- Form 10F

- Agreement/Invoice

- Beneficial ownership declaration

Property Transactions Involving Non-Residents

Real estate transactions continue to be a high-risk area for TDS non-compliance.

Key Points:

- TDS is deducted on gross sale consideration, not capital gains

- Buyer is responsible for TDS deduction

- Rates vary based on holding period

Upcoming Simplification (October 2026)

- PAN-based compliance system to simplify TDS procedures

- Reduced documentation burden for buyers

Major Risk Areas to Avoid

Failure in compliance can result in interest, penalties, and disallowance of expenses.

Common Mistakes:

- Incorrect section reference (old vs new law)

- Failure to deduct TDS

- Late deposit or filing delays

- Ignoring DTAA provisions

- Incomplete or missing documentation

A structured compliance checklist is essential for organizations dealing with foreign payments.

Practical Impact on Businesses & Professionals

The new TDS regime requires:

- Stronger internal controls

- Coordination with tax advisors

- Timely documentation and verification

For startups, MSMEs, and professionals dealing with international vendors, this change introduces both compliance challenges and planning opportunities.

Conclusion: Compliance is the New Tax Strategy

The Non-Resident TDS changes effective April 1, 2026, mark a significant evolution in India’s international taxation framework. While the rates remain familiar, the procedural and documentation requirements have become more structured and stringent.

Businesses that proactively adapt to:

- Updated sections

- New forms

- DTAA documentation

- Timely compliance

will not only avoid penalties but also optimize tax outflows and improve cash flow efficiency.

In the evolving global tax ecosystem, compliance is no longer optional—it is a strategic advantage.

Team: CreditMoneyFinance.com

More Featured Posts:

The Ultimate Guide to Company Registration in Dubai 2026: Benefits, Compliance, and Costs.

Collateral-Free Business Loans in India: A Complete Guide for SMEs & Startups (2026 Edition).

The Strategic Role of Venture Capital and Private Equity in the Global Startup Ecosystem.

Breaking the Ceiling: 10 IPO Myths Holding SME Promoters Back.

Why MSMEs Trust Us With Their Most Critical Financial Decisions