RBI Tightens Credit Information Reporting Norms from 1 July 2026: What Banks, NBFCs, Businesses and Borrowers Must Know.

The Reserve Bank of India has introduced new Credit Information Reporting norms effective 1 July 2026. Learn about four monthly reporting cycles, incremental reporting, stricter compliance timelines, improved credit score updates, and the impact on banks, NBFCs, businesses, and borrowers.

RBI Introduces a New Era of Credit Information Reporting

In a significant step towards strengthening India’s credit ecosystem, the Reserve Bank of India (RBI) has implemented a comprehensive overhaul of the Credit Information Reporting framework with effect from 1 July 2026.

The revised framework aims to improve the accuracy, consistency, transparency, and timeliness of credit information shared by banks, Non-Banking Financial Companies (NBFCs), and other regulated lending institutions with Credit Information Companies (CICs).

These reforms are expected to benefit lenders, borrowers, regulators, and the overall financial system by ensuring that credit information is updated more frequently and accurately than ever before.

Why Did RBI Introduce These Changes?

India’s credit ecosystem has grown rapidly over the past decade with increasing digital lending, fintech innovations, personal loans, MSME financing, and retail credit expansion.

However, delayed reporting and inconsistent data often resulted in:

- Incorrect credit scores

- Delayed reflection of loan repayments

- Errors in borrower records

- Wrong overdue reporting

- Delayed loan approvals

- Customer grievances

The RBI’s latest framework addresses these concerns by introducing a standardized and technology-driven reporting mechanism.

Major Changes Effective from 1 July 2026

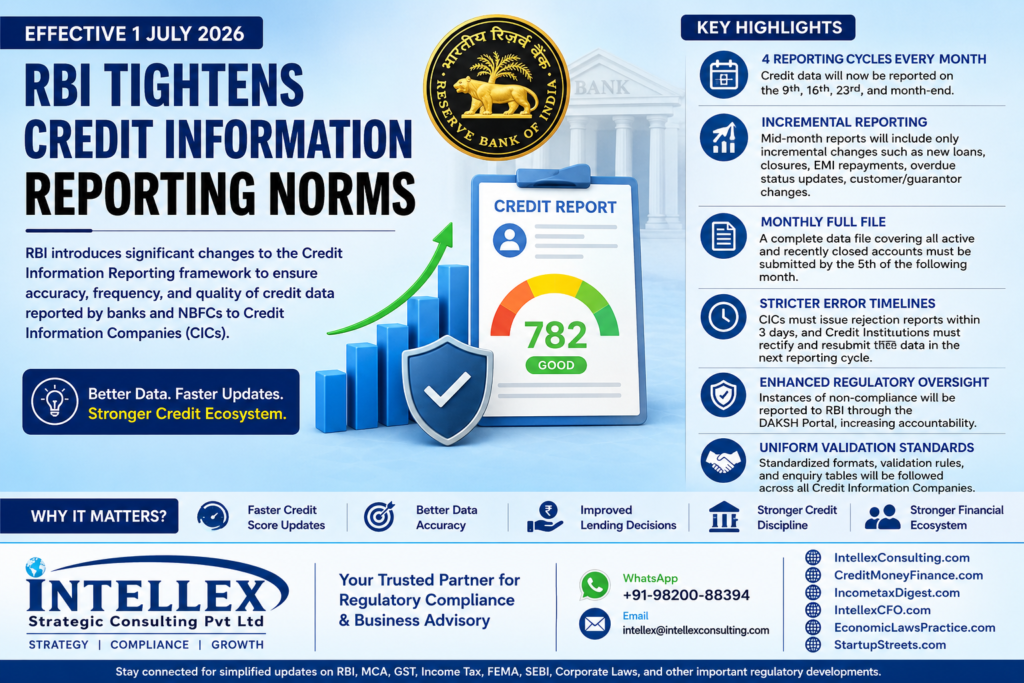

1. Four Credit Reporting Cycles Every Month

One of the biggest changes is the increase in reporting frequency.

Earlier, lenders generally submitted data on a fortnightly basis.

Now, every Credit Institution must report data on:

- 9th of every month

- 16th of every month

- 23rd of every month

- Last day of every month

This means credit information will be refreshed much more frequently.

Benefits

- Faster credit score updates

- Reduced reporting delays

- Better visibility of borrower behaviour

- Quicker correction of account status

2. Introduction of Incremental Reporting

Instead of sending the entire database every reporting cycle, institutions will now submit only incremental changes during mid-month reporting.

These include:

- Newly sanctioned loans

- Fresh credit card issuances

- Loan closures

- EMI payments received

- Overdue updates

- Changes in customer information

- Guarantor modifications

- Settlement updates

- Account restructuring

- Write-offs and recoveries

This significantly reduces processing time while ensuring timely updates.

3. Monthly Full File Submission

Apart from incremental reporting, every Credit Institution must submit one comprehensive data file each month.

The complete file must include:

- All active loan accounts

- Recently closed accounts

- Credit card accounts

- Borrower details

- Guarantor information

- Outstanding balances

- Credit limits

- Account status

The full file must be submitted by the 5th day of the following month.

This helps maintain database integrity across all Credit Information Companies.

4. Stricter Error Rectification Timeline

The revised framework introduces stringent timelines for correcting reporting errors.

Credit Information Companies (CICs)

- Must validate submitted data immediately

- Issue rejection reports within 3 days

Banks and NBFCs

- Must rectify errors promptly

- Resubmit corrected information in the very next reporting cycle

This significantly reduces prolonged inaccuracies in borrower records.

5. Uniform Validation Standards

Earlier, different Credit Information Companies often followed varying validation procedures.

The RBI has now standardized:

- File formats

- Validation rules

- Data fields

- Error codes

- Enquiry formats

- Reconciliation mechanisms

This creates consistency across all Credit Information Companies operating in India.

6. Enhanced Regulatory Oversight

The RBI has strengthened compliance monitoring through the DAKSH Portal.

Instances of:

- Delayed reporting

- Incorrect reporting

- Non-submission

- Repeated validation failures

- Data quality issues

may now be reported to RBI through the DAKSH supervisory platform.

This increases accountability among regulated entities.

Impact on Banks

Banks will now need to invest in:

- Better core banking integration

- Automated reporting systems

- Data quality controls

- Compliance monitoring

- Real-time reconciliation

Operational teams will require stronger coordination between:

- Credit departments

- IT teams

- Compliance functions

- Operations

- Risk management

Impact on NBFCs

NBFCs may experience a larger compliance burden, particularly smaller institutions.

They will need to ensure:

- Accurate customer records

- Timely EMI updates

- Automated reporting

- Better system integration

- Faster correction of rejected records

However, these changes also improve their credibility within the lending ecosystem.

Benefits for Borrowers

The revised framework is highly beneficial for borrowers.

Faster Credit Score Updates

EMI payments and loan closures will reflect much earlier.

Better Loan Eligibility

A quicker update of repayment history may improve credit scores sooner.

Reduced Reporting Errors

Incorrect overdue reporting can be corrected more efficiently.

Faster Loan Approvals

Lenders will have access to fresher credit information.

Greater Transparency

Borrowers can expect more accurate credit histories.

Benefits for Financial Institutions

Financial institutions will benefit through:

- Better credit underwriting

- Reduced fraud risk

- Improved portfolio monitoring

- More reliable borrower information

- Enhanced risk assessment

- Lower credit losses

Importance of Accurate Data

The RBI has emphasized that data quality is just as important as reporting frequency.

Institutions must ensure accuracy in:

- PAN

- Aadhaar-linked identity details (where applicable)

- Customer name

- Date of birth

- Address

- Mobile number

- Loan amount

- Outstanding balance

- Repayment status

- Default history

- Guarantor details

Even minor inaccuracies can lead to validation failures.

Digital Transformation in Credit Reporting

The revised framework encourages:

- Straight-through processing

- API-based reporting

- Automated reconciliation

- Digital audit trails

- Standardized compliance

This aligns with India’s broader digital financial infrastructure.

Practical Tips for Borrowers

Borrowers should:

- Pay EMIs on time.

- Regularly check their credit reports.

- Report inaccuracies immediately.

- Keep KYC records updated.

- Inform lenders about changes in contact details.

- Monitor loan closure updates.

- Preserve loan repayment records.

Compliance Checklist for Banks and NBFCs

Financial institutions should:

- Upgrade reporting systems.

- Validate customer master data.

- Establish automated reporting workflows.

- Monitor rejection reports daily.

- Ensure timely rectification.

- Train compliance and operations teams.

- Conduct periodic internal audits.

- Maintain complete documentation.

Conclusion

The RBI’s revised Credit Information Reporting framework marks a significant milestone in strengthening India’s financial infrastructure. By increasing reporting frequency, introducing incremental reporting, standardizing validation procedures, enforcing stricter correction timelines, and enhancing regulatory oversight, the new regime is expected to improve the quality and reliability of credit information across the country.

For borrowers, this means faster credit score updates and more accurate credit histories. For banks and NBFCs, it reinforces the importance of robust data governance and timely compliance. Ultimately, these reforms will contribute to a more transparent, efficient, and trustworthy credit ecosystem, supporting responsible lending and healthier financial growth.

Need Professional Assistance?

Intellex Strategic Consulting Pvt Ltd provides expert advisory and compliance support in RBI Regulations, Banking Compliance, NBFC Advisory, FEMA, SEBI, MCA, GST, Income Tax, Corporate Laws, Startup Advisory, Risk Management, and Regulatory Compliance.

Contact Us

Intellex Strategic Consulting Pvt Ltd

📱 WhatsApp: +91-98200-88394

📧 Email: intellex@intellexconsulting.com

🌐 IntellexConsulting.com

🌐 CreditMoneyFinance.com

🌐 IncometaxDigest.com

🌐 IntellexCFO.com

🌐 EconomicLawsPractice.com

🌐 StartupStreets.com

Stay connected for simplified updates on RBI, MCA, GST, Income Tax, FEMA, SEBI, Corporate Laws, and other important regulatory developments affecting businesses and professionals across India.

Intellex Strategic Consulting Pvt Ltd

More Featured Articles:

Strategic Investment for High-Growth Companies in India – Family Office Funding

Venture Debt in India: The Complete 2026 Guide for Startups, Founders, CFOs & Growth Companies.

How Startups Can Raise Funding in Dubai: A Comprehensive Guide for Founders and Entrepreneurs.