RBI Amendment Directions 2026 on NBFC Registration & Scale-Based Regulation: What Every NBFC Professional Must Know.

RBI’s 2026 amendment to NBFC Registration and Scale-Based Regulation introduces Type I, Type II and Unregistered Type I NBFC classifications. Learn key compliance changes, deregistration process, exemptions, and actionable insights for NBFC professionals.

Introduction

The Reserve Bank of India (RBI) has introduced a critical regulatory update through Circular RBI/2026-27/43 dated April 29, 2026, amending the NBFC Registration, Exemptions and Scale-Based Regulation Directions, 2025. These changes, effective July 01, 2026, significantly reshape how certain NBFCs are classified, regulated, and potentially exempted from registration.

For professionals working in or advising NBFCs, this amendment is not just procedural—it directly impacts classification, compliance strategy, and regulatory exposure.

Background: Why This Amendment Matters

Historically, NBFCs that did not accept public funds and had no customer interface operated in a grey regulatory space. While they were recognized in practice, there was no formal classification, leading to ambiguity in compliance and supervision.

The RBI has now addressed this gap by:

- Introducing clear categorisation

- Providing a formal exemption framework

- Strengthening accountability mechanisms

This ensures regulatory clarity while maintaining oversight.

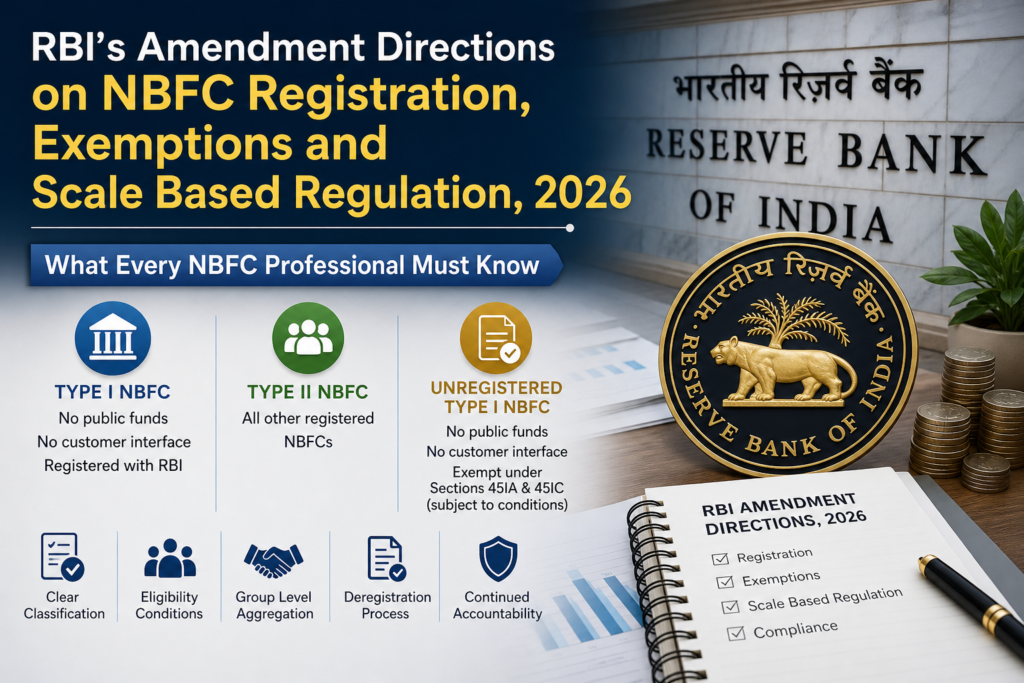

New Classification Framework for NBFCs

The amendment introduces three distinct categories:

1. Type I NBFC

- Does not avail public funds

- Has no customer interface

- Is registered with RBI

- Holds a valid Certificate of Registration (CoR)

2. Type II NBFC

- Covers all other registered NBFCs

- Includes entities with:

- Public funds

- Customer interface

- Higher regulatory exposure

3. Unregistered Type I NBFC

This is the most significant introduction.

These are entities that:

- Do not avail public funds

- Do not have customer interface

- Are exempt from registration under Sections 45IA and 45IC of the RBI Act, 1934

- Must comply with specific eligibility conditions

Eligibility Criteria for Unregistered Type I NBFC

To qualify, an NBFC must satisfy all four conditions simultaneously:

✅ 1. Business Model Commitment

- Must operate without public funds and customer interface

- This must be a conscious and long-term strategy

✅ 2. Asset Size Threshold

- Total assets must be below ₹1,000 crore

- Based on latest audited financial statements

✅ 3. Annual Board Resolution

- Mandatory resolution at the start of every financial year

- Confirming:

- No public funds

- No customer interface

✅ 4. Disclosure Requirements

- Notes to Accounts must explicitly disclose:

- Status as Unregistered Type I NBFC

- Position on public funds and customer interface

Group-Level Aggregation Rule: A Critical Compliance Trigger

A major compliance risk arises at the group level.

👉 If multiple Unregistered Type I NBFCs exist within a group:

- Their asset sizes must be aggregated

- If combined assets ≥ ₹1,000 crore:

- All entities must register with RBI

- Classification shifts to Type I NBFC

This prevents regulatory arbitrage through fragmentation.

Deregistration Opportunity for Existing NBFCs

The RBI provides a one-time strategic opportunity:

Who Can Apply?

- Existing NBFCs:

- Without public funds

- Without customer interface

- Including those already registered as Type I NBFCs

Deadline

📅 December 31, 2026

Application Platform

- RBI’s PRAVAAH Portal

Documentation Required

- Original Certificate of Registration (CoR)

- Audited financial statements (last 3 years)

- Declaration of public funds & customer interface status

- Statutory Auditor’s Certificate

- Board Resolution confirming future intent

Important: Exemption is Limited, Not Absolute

A common misconception is that exemption equals deregulation. That is not true.

Even Unregistered Type I NBFCs:

- Remain governed under Chapter IIIB of the RBI Act, 1934

- Are subject to RBI directions and inspections

- Can face regulatory action under Chapter V

Enhanced Role of Statutory Auditors

Auditors now play a direct regulatory reporting role:

- Must issue an Exception Report to RBI

- Required if:

- Entity violates conditions

- Uses public funds

- Develops customer interface

This increases compliance accountability and early risk detection.

Practical Implications for NBFC Professionals

This amendment demands immediate strategic evaluation.

Key Action Points

✔️ Classification Assessment

Determine whether your NBFC falls under:

- Type I

- Type II

- Unregistered Type I

✔️ Deregistration Strategy

Evaluate:

- Cost-benefit of remaining registered

- Operational flexibility vs regulatory oversight

✔️ Board Governance Strengthening

Ensure:

- Annual resolutions are timely and properly documented

✔️ Financial Reporting Compliance

Update:

- Notes to Accounts disclosures

- Internal compliance checklists

✔️ Group Structure Review

Assess:

- Aggregate asset exposure

- Risk of crossing ₹1,000 crore threshold

Strategic Insight: Compliance as a Competitive Advantage

Forward-looking NBFCs will use this amendment to:

- Simplify regulatory burden (via deregistration where appropriate)

- Enhance governance credibility

- Avoid future enforcement risks

In a tightening regulatory environment, proactive compliance is not a cost—it is a strategic asset.

How We Can Help

At Intellex Strategic Consulting Pvt Ltd, we assist NBFCs in navigating complex regulatory landscapes with precision and clarity.

Our Services Include:

- NBFC classification and regulatory diagnostics

- Deregistration advisory and end-to-end execution

- RBI compliance audits and readiness assessments

- Board governance frameworks and documentation

- Financial disclosures and regulatory reporting support

Contact Us

📞 WhatsApp: +91-98200-88394

📧 Email: intellex@intellexconsulting.com

🌐 Websites:

- IntellexConsulting.com

- IntellexCFO.com

- EconomicLawsPractice.com

- CreditMoneyFinance.com

Conclusion

The RBI’s 2026 amendment is a landmark clarification in NBFC regulation, particularly for entities operating without public funds or customer interface.

It introduces clarity, flexibility, and accountability but also demands disciplined compliance execution.

For NBFC professionals, the message is clear:

Understand, evaluate, and act well before the deadlines.

Intellex Strategic Consulting Pvt Ltd

More Featured Compliance Posts:

RBI FLA Return 2026: Compliance Challenges for GIFT IFSC Entities Under FEMA Explained.

The Ultimate Guide to Company Registration in Dubai 2026: Benefits, Compliance, and Costs.

Ultimate Guide to Singapore Company Registration 2026: Rules, Costs, and Compliance

Expert Guidance on Compliance for Private Limited Companies and LLP in India

Expert Accounting & Taxation and Statutory Compliances Solutions across Indian Cities